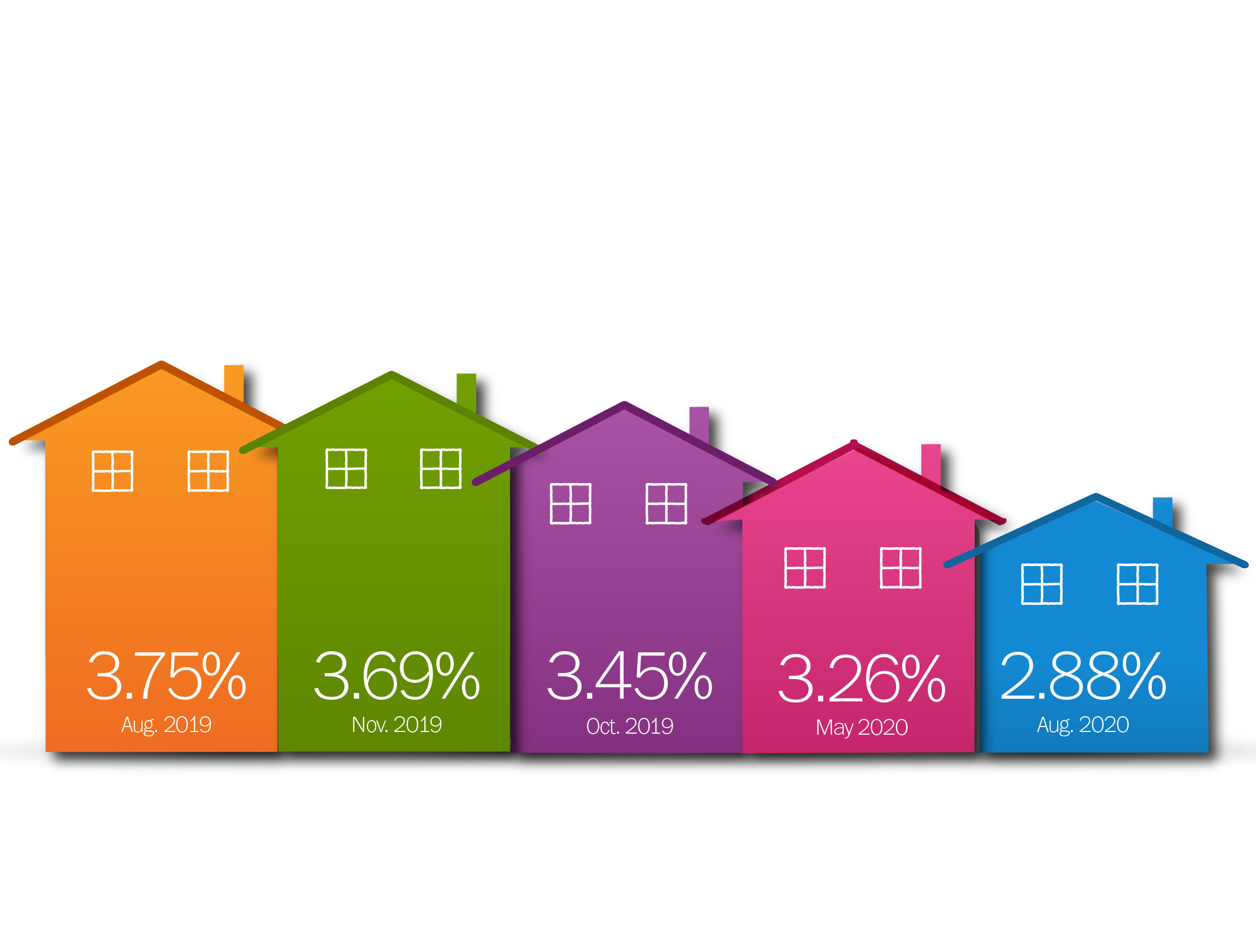

This is just one of one of the most usual reverse home mortgage troubles that just isn't true. You remain to own your house, hold title and also have complete control over it, just as you would with a regular home mortgage. The financial institution can not force you to market and you can live there as long as you desire. Your only responsibility is to keep your home well-maintained as well as pay your real estate tax as well as insurance. Reverse mortgage loan providers usually charge a source cost as well as various other closing expenses, along with maintenance costs over the life of the mortgage. Some likewise charge home loan insurance policy costs (for federally-insured HECMs).

Now, you need not assume by this article that I have anything against you using a reverse home mortgage or that I believe they are a poor item and those that sell them ought to obtain some cement shoes. If you really understand exactly how a reverse mortgage jobs and also still want to use one, I do not have a trouble with that. But one of the most effective means to recognize something is to see the troubles with it.

- The downside to a reverse home loan is that you are using your residence's equity while you are alive.

- In a lot of the reported frauds, victim elders are provided complimentary residences, investment opportunities, and also repossession or refinance assistance.

- No settlements are due on a reverse home mortgage until some trigger event, such as vacating the house or fatality of the debtor.

The finance does not have to be paid back as long as you reside in the house. Nonetheless, the finance will certainly become due when you pass away, stop working to pay tax obligations or insurance for the home, let the home fall into disrepair, or offer the home or no more use the residence as your primary residence. The lender can not sue you or your estate for the lending balance, yet it can sell the house. Never ever let a lender stress or rush you with the process. Make certain you comprehend the features and total expense of a reverse home loan before authorizing anything. That changes, however, if you market or move out of the house, or if you pass away.

What Is Shared Recognition As Well As Equity Engagement?

They need to be used to pay for a particular, lender-approved thing. This is typically the most cost effective sort of reverse home mortgage. Regrettably, too many individuals delayed choices concerning their future economic health too long.

Pros Of A Reverse Home Loan

Your beneficiaries have 1 month from obtaining the due and payable notice from the lending institution to get the home, market the home, or transform the residence over to the lender to satisfy the financial obligation. However, it may be how to get rid of timeshare without ruining credit feasible for the timeline to be prolonged approximately a year so that your beneficiaries can sell the home or obtain financing to purchase the home. Your beneficiaries can get in touch with a HUD-approved housing therapy agency or a lawyer to learn more.

Contrast By Credit History Required

In in between those, there's a lot of area for reasonable people to disagree. It's primarily all academic anyhow, considering that you as well as I aren't mosting likely to use can timeshare estates be passed down to heirs one. But I 'd allow someone advertise them on the site, unlike whole life insurance. It's smarter than a lot of points individuals do while trying to obtain even more income out of their how to cancel a timeshare contract in florida nest egg. Thx for what I consider an even more balanced message on it.